Universal health coverage: what it is, progress and pitfalls along the way

- Page updated onJune 29, 2026

Universal health coverage consists of all people having access to the set of quality health services they need, when and where they need them, without suffering financial hardship. This goal is today adopted by countries and global health actors of all kinds in their policies and reforms; moreover, it constitutes Sustainable Development Goal 3.8.

In practice, each country starts from a completely different situation and faces completely different difficulties in pursuing universal health coverage, so there are large differences in the results they achieve. Moreover, in recent years, not only has service coverage not improved in many of these countries, but catastrophic out-of-pocket health expenditures have increased significantly. Faced with these problems, governments sometimes take alternative shortcuts to the essential principles of universal health coverage that can be fraught with pitfalls.

Table of contents:

What is universal health coverage?

Twenty years pushing for more equitable health financing

In the last twenty years there have been major milestones that have driven the adoption of goals related to universal health coverage. These include resolution 58.33 of the 2005 World Health Assembly. This was the first time that member states were clearly urged to invest in prepayment and develop health financing models based on pooling funds and sharing risks. The reason? To reduce reliance on out-of-pocket payments, which create inequity and poverty.

This resolution was followed by the World Health Report 2010. It details how countries can modify their health financing models to move towards universal coverage and how international cooperation actors can support the poorest countries in doing so.

From this moment on, many other reports, positions, policies and alliances for universal health coverage appeared.

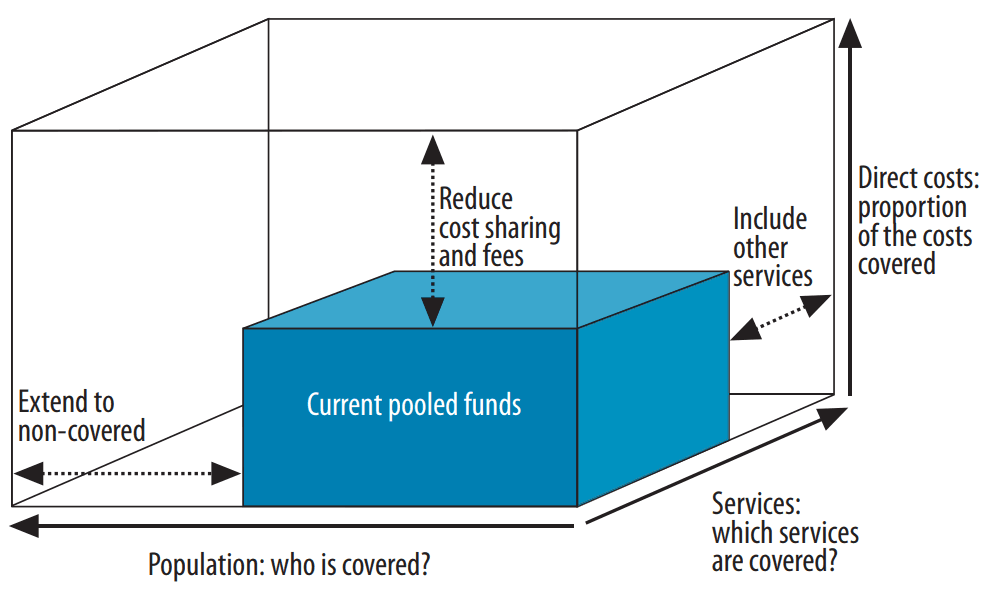

Universal health coverage has three dimensions

According to this model, the way to achieve universal health coverage is to take the necessary steps to ensure that:

- The pooled funds cover all health care expenses, so that no out-of-pocket expenses are left to be covered by out-of-pocket payments.

- For all possible health services that may be necessary throughout the life span, including promotion, prevention, diagnosis, treatment, rehabilitation and palliative care.

- For all people, including both those who contribute to these pooled funds through taxes and contributions and those who, because they are poor, cannot make contributions of any kind.

There can be no universal health coverage if the national health insurance system leaves out part of the population because they are unable to contribute to the pooled funds. Nor can there be universal health coverage if users have to pay directly a large part of the direct costs of the health care they receive. Finally, neither can this goal be achieved if the network of services and their accessibility are not sufficient for rural and dispersed areas, or if the quality of services is not sufficient to solve health problems, for example.

Therefore, each country must critically analyze the volume of its "blue box" of pooled funds, in what dimension or dimensions it is farthest from achieving universality and what steps it must take to reach it and maintain it over time.

The different paths to universal health coverage

In the richer countries, national health insurance came with industrialization.

The Industrial Revolution of the 18th and 19th centuries brought about a change in the way health was understood in some nations, as a collective good necessary for productivity and development. Authorities in highly industrialized societies such as Germany, France, Russia, Japan or the Russian Empire (even before the existence of the Soviet Union) understood that for the economy to advance, workers needed adequate insurance against injury and illness, contracted through employers or directly with the State. Thus, the first ideas of population-based health coverage were almost a "natural" result of the technological and economic advances of the time. These initiatives were consolidated in the second half of the 20th century in most of these countries, after World War II, with the introduction of national health services and universal health care systems.

In one way or another, all these countries -with the well-known exception of the United States-, at some point, decided to develop prepayment schemes for the entire population (through tax revenues or mandatory contributions from employers and employed persons) as the main approach to their health systems. Today, the main threats to universal health coverage in these countries lie in the discriminatory policies that exclude undocumented migrants or unemployed people, in the influence of the private sector that undermines the financial sustainability of the public sector, and in the interests of political parties that try to socially delegitimize the public health system.

Democracy also brought reforms, but with greater underlying inequality

In many other countries, a second wave of reforms in national health systems toward universal health coverage occurred with the advent of their democracy in the 1980s and 1990s. This is the case in many Latin American countries and the Philippines, for example.

However, the factors driving health reform in these countries and their starting situation were very different from those of the first group. As a result, the resulting dynamics and health systems were also very different. The common feature in these countries was the inequality among large segments of the population in their access to health care and the strong penetration of the private sector in both health care delivery and insurance management.

In the poorest countries, change has yet to occur

At the beginning of the 21st century, a third wave of health reforms towards universal health coverage began in the countries lagging furthest behind. This coincided with the launch of the Millennium Development Goals in 2000, which included targets related to universal access to maternal health services. It was also the time when new global health initiatives related to HIV/AIDS saw the light of day and a subsequent - relative - shift in their focus to health systems support. With all this, the discourse of universal health coverage began to permeate political forums, declarations and speeches.

This latter group of nations includes many sub-Saharan African countries. In them, new social safety nets and welfare systems aimed at achieving universal health coverage have only recently begun to be launched. These countries, however, have much fewer economic resources than those of European, Asian and Latin American countries when they launched their respective systems. This marks important limitations in the achievements they attain. In addition, they start from health systems with significant weaknesses in development, regulation, human resources, and equipment. Their public administrations also have poor fiscal capacity to collect taxes and contributions to support public investment in health.

🧠 Let's pause and reflect

Think about each of the three dimensions of universal health coverage (population, services, and direct costs covered). What challenges might exist in a complex humanitarian crisis context to advance in each of them?

- 1Think and write your answer.

- 2Click on «Copy and open».

- 3Paste to receive feedback.

📚 This is the NotebookLM for this topic. It uses only carefully selected references. | What is NotebookLM?

Is there universal health coverage in the world today?

Current levels of service coverage and financial hardship

Although there has been evident progress, progress has slowed since 2015. Moreover, uncertainty for 2026 and beyond is at its highest because of cuts in international aid and the health workforce crisis. The global UHC service coverage index increased from 54% in 2000 to 68% in 2015, but by 2023, only 71% had been reached, and it is estimated that we will not pass 74% in 2030. Today, 4.6 billion people lack full access to essential health services. If we also disaggregate this access by type of health service, we also see the stagnation of maternal and child health, reproductive and sexual health, and that non-communicable diseases continue to lag far behind.

In terms of financial protection against health spending, there have also been improvements, but much more timid and now also slower. The percentage of world population incurring financial hardship due to out-of-pocket health spending fell from 34% in 2000 to 26% in 2022, and is not expected to fall below 24% in 2030. Put another way, today it is estimated that in 2030, one in 4 people on the planet will face large and impoverishing health spending. The data also show that the biggest determinant of high out-of-pocket health spending is medicines, accounting for 60% of the health spending of the poorest households.

Implications for public health policy

Although the above data should be interpreted according to the specific figures, context and health system of each country, there are key implications that are relevant to all of them. These include the priority of guaranteeing free health care for the poorest people, strengthening prepayment schemes, focusing on reducing out-of-pocket spending on medicines and ensuring that health services for non-communicable diseases are not neglected.

The 2025 UHC global monitoring report also highlights the importance of political commitment to primary health care and multisectoral policies, avoiding inadequate shortcuts that compromise health equity. Besides, other initiatives highlight that having beautiful UHC-oriented health policies is not enough, when one-third of the countries do not actively monitor whether progress is being made.

Pitfalls along the way to universal health coverage

The road to achieving universal health coverage is difficult and full of obstacles. For this reason, countries often try to take inadequate paths full of pitfalls, which can even undermine equity and the population's right to health.

Financing is not everything

There is a first risk related to a limited vision of universal health coverage that limits its vision to a logic of financing health services, without properly understanding financing as one more pillar of the health system, without embracing the valuable principles and values of the primary health care strategy, and without recognizing the vital importance of the social determinants of health (universal health coverage being one of them).

Market logic in healthcare generates inequity

Both the WHO and the World Bank have insisted on the need for private sector participation in the provision of services and insurance in middle- and low-income countries. The WHO justifies this on the grounds that such companies already exist and have a high penetration in these countries. For its part, the World Bank defends it with a neoliberal economic logic. However, a large share of the private for-profit sector in a health system is an enormous risk.

Evidence indicates that health systems governed by market logic are less equitable. In them, the poorest people receive fewer benefits. They are also less efficient. This is partly due to the huge administrative costs devoted to controlling that only health interventions implemented according to certain clinical standards are covered, and to the interest of companies in generating profit. Finally, they are more difficult to govern towards health equity and public health priorities. When there are powerful business lobbies, they try to impose their agenda.

However, the use of mixed public-private models is a reality in many contexts. In these, accountability, transparency, leadership from the public sector and citizen participation are especially important to ensure respect for the principles of universal health coverage.

Fragmentation widens the gap in coverage between rich and poor

When there are multiple payers, funds or different insurances, the system becomes fragmented. In these cases, a private system for the rich coexists with a system of social insurance for the middle class and a minimum package of services for people with fewer resources covered by public funds. As a result, people with higher incomes do not share risks or contribute to cover the health costs of poorer people with more health problems.

However, in single-payer models, citizens make contributions to a pooled fund generally managed by the state, which is responsible for making payments to healthcare providers (whether public or private). The results can be even better when the single-payer model is combined with a capitation payment system, in which the government pays a fixed amount per person. This avoids incentivizing more procedures or payments to be made than necessary. This model reduces administrative costs and better equalizes the risks and benefits for the entire population, contributing to the equity and sustainability of the system.

Financing based on voluntary contributions cannot be universal

In some low-income countries, the authorities have opted to promote systems with financing based on voluntary contributions rather than public revenue sources. This, however, is also unfeasible for the achievement of universal health coverage.

This is the case, for example, in African countries that establish common social insurance only for a small proportion of the population (generally military and civil servants of a certain level). In doing so, they leave the health coverage of the rest of the population dependent on voluntarily adhering to community health insurance, usually fragmented across multiple geographic areas. This alternative is often promoted as a «realistic approach» in contexts where the majority of the population does not have a formal job that allows for sustainable collection of contributions and certain taxes. This model, under certain conditions, can indeed help increase the use of health services and reduce out-of-pocket payments among its members. However, it excludes the most vulnerable people, who cannot afford to pay their membership fees, thus deviating from population public health priorities and health equity.

The system must cover the entire population and this requires in many cases an increase in public investment in the health sector. Supporting community health insurance initiatives without at the same time advocating for additional public funding to guarantee access to quality health care for the poorest produces discrimination.

Limiting benefit plans cannot be the solution

In some contexts it is common to try to reduce benefit plans to a minimum set of services considered a priority, to be implemented following specific clinical guidelines. However, in practice, this is really difficult to do. In addition, it involves high costs for evaluating each case and approving insurance coverage, generates tensions between insurers and healthcare personnel, and raises barriers for users. Many of them will choose not to use certain services if they do not know with certainty that they will be covered by their insurance.

However, no country can simply «cover everything». Therefore, on the one hand, it is key to advocate for strategic purchasing of health services. This is the process by which authorities allocate funds to selected health care providers to deliver selected health services under established payment mechanisms. Strategic purchasing of health services should always prioritize cost-effective services (which requires prioritization of primary care), and that they are implemented from a vision of equity and public health, taking into account the needs of all people, including the most vulnerable and needy.

On the other hand, this vision must, of course, include additional effective strategies to reduce costs and improve the efficiency of the system without reducing its effectiveness. This includes the fight against corruption, the promotion of generic drugs, the promotion of rational prescribing, incentives for good performance, improved hospital planning, periodic quality assessment, improved management and regulation, etc.

NotebookLM

You can review my bibliographic references on universal health coverage with this NotebookLM, an artificial intelligence-based research assistant. Do you want to know more?

How to cite this page

Abarca, B. (June 29, 2026). Universal health coverage: what is it, progress and pitfalls along the way?. Salud Everywhere. https://saludeverywhere.com/en/health-in-humanitarian-crises/universal-health-coverage/

External links

- UHC 2030, 20225. ACT for UHC 2025 Report.

- WHO, World Bank, 2025. Tracking Universal Health Coverage: 2025 Global monitoring report.

- People’s Health Movement, 2023. The Universal Health Coverage / Primary Health Care divide. Global Health Watch 6 report.

- WHO, World Bank, 2023. Tracking Universal Health Coverage: 2023 Global monitoring report.

- UHC2030, 2023. From commitment to action. Action agenda on universal health coverage from the UHC movement.

- United Nations, 2019. Political declaration of the high-level meeting on universal health coverage.

- People’s Health Movement, 2016. Priority setting for universal health care.

- People’s Health Movement, 2014. The current discourse on Universal Health Coverage (UHC). Global Health Watch 4 report.

- Kutzin, 2012. Anything goes on the path to universal health coverage? No.

- WHO, 2010. The World Health Report 2010

Health Systems Financing: the Path to Universal Coverage. - World Health Assembly, 2005. WHA58.33. Sustainable health financing, universal coverage and social health insurance.